Pay More, Own Less and Inherit the Debt

The Silent Squeeze: How a Generation Was Gaslit by the Tax System

Every year, hundreds of billions are silently transferred from working people to wealth holders, retirees, and creditors - with no consent and no upside.

Here’s how it works:

£572 billion in personal taxes were paid by working-age Brits in 2023–24, including 100% of National Insurance.

£319 billion in welfare went mostly to retirees including pensions, benefits, and care of which the working-age citizens of the UK rarely receive.

Housing equity gains are untaxed, while renters face c.30% real-terms increases since 2014.

£78 billion/year is spent just on interest payments to bondholders, which is more than education or policing.

Our reward? Longer working lives, higher taxes, and a future mortgaged to pay for past promises.

How We Got Here

Since the early 2000s, UK policy has quietly shifted from shared prosperity to intergenerational extraction enabled by stealth taxes, frozen thresholds, and political cowardice.

Tax burden: Now 37.5% of GDP, the highest in modern UK history.

(Up from ~33% pre-2010. OBR projects 38%+ by 2028.)Fiscal drag: Income tax thresholds frozen until 2028, pulling millions into higher tax bands without rate increases.

Triple lock pensions: Outpaced wage growth since 2010. Pensioners now receive ~£10,000/year more in net transfers than they contribute.

Public investment flatlined: Education, transport, and housing spend per capita fell in real terms, even as debt interest doubled.

Debt interest in 2023–24: £78bn - larger than the entire school system.

Here's a timeline graphic showing the UK's structural fiscal drift (2000–2024):

The UK tax burden is increasingly rising toward record highs:

Debt interest spiking post-2021, now consuming more than education.

Pensioner net benefit growing nearly 3x, while working-age benefits stagnate.

The Invisible Tax Hike

Income tax thresholds have been frozen until 2028 which is dragging millions into higher tax brackets as wages rise with inflation. In 2022, the UK froze all major personal income tax thresholds, and extended the freeze to April 2028.

This means:

More people pay basic tax

More pay higher-rate tax

Personal allowance stays flat at £12,570 while inflation eats into take-home pay

As a result, by 2028:

Over 4 million more people will pay income tax

3 million more will be dragged into higher-rate brackets

The government will raise £40–50 billion in stealth taxes without changing a single headline rate

A worker earning £35K in 2022 with 4% annual wage growth ends up paying ~£1,200 more in income tax by 2026, even though the tax rates never changed. Their “pay rise” mostly vanishes in higher tax take and poorer services, meanwhile, thresholds stay frozen, and take-home pay stagnates in real terms.

Work is Taxed. Wealth is Protected.

The tax system rewards owning assets, not earning income, and it’s costing the average individual in the UK thousands every year.

Income tax & NICs: Workers pay up to 42% on earnings over £50K (incl. NICs).

Capital gains tax (CGT): Max 24%, often lower, and you can deduct inflation.

Main homes are CGT-exempt.

Property wealth rises tax-free, even if our rent does not.

Pensioners pay 0% NICs, even on six-figure incomes.

Dividend tax: Lower than income tax. Capital earns more, taxed less.

The Housing Trap

A system built on rising house prices, tax-free gains, and intergenerational inequality funded by your income, rent, and future debt. Homeownership among under-35s is down from 65% (1997) to 35% today. The stats are astounding:

Average first-time buyer age: 34 (vs 26 in 1997, and rising)

Property wealth gains are CGT-exempt on main residences.

Renters pay ~30% of post-tax income on rent, often more in London & SE.

Landlords can deduct mortgage interest + costs. Renters can’t deduct rent.

Council tax is regressive - a £20M mansion often pays less than a 3-bed flat in Manchester.

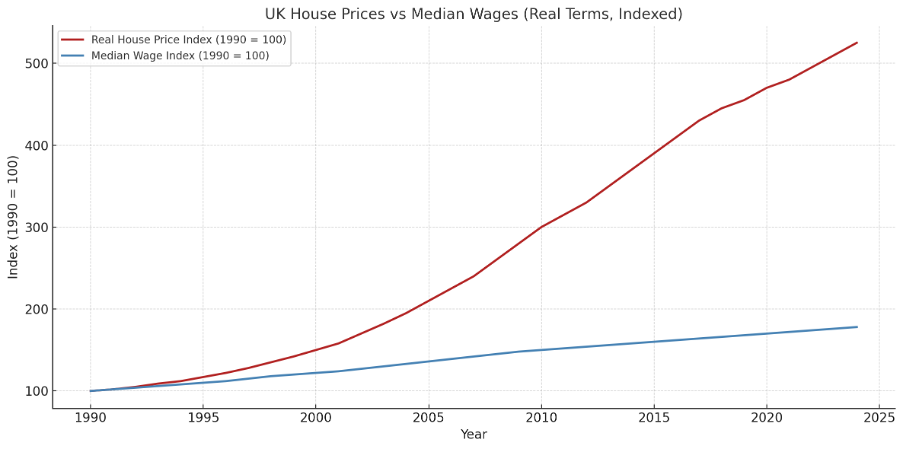

UK House Prices vs Median Wages (Real Terms, Indexed)

Real house prices have increased by over 400% since 1990, whereas median wages have grown just ~80% in the same period. It is unsustainable to stay on this course.

The Pension & NIC Scam

The National Insurance Contributions (NICs) system is structured to collect a percentage of earnings from the working-age population. Employees contribute approximately 12% of their earnings, while employers contribute an additional 13.8% on behalf of their workers. However, pensioners are entirely exempt from paying NICs, even if they continue to earn significant incomes, such as £100,000 or more annually after retirement.

The State Pension for the 2023–24 financial year offers a full rate of £221.20 per week, amounting to over £11,500 per year. This amount is protected under the "triple lock" system, ensuring that it rises each year in line with the highest of inflation, average wage growth, or 2.5%. Therefore, it is safeguarded against economic fluctuations, including wage decreases or potential government cuts.

In the 2023–24 period, NICs generated a total revenue of £159 billion, which was paid almost entirely by individuals of working age. Meanwhile, spending on state pensions exceeded £125 billion annually, a figure that continues to grow at a rate faster than the overall growth of the economy (GDP). Adjusted for taxes, this results in a net annual transfer of wealth to the 65+ age group, amounting to an estimated £120–150 billion.

We are paying taxes on every payslip to fund pensions for people who pay no tax on theirs, and perhaps most importantly vote to keep it that way.

Debt Interest: The Black Hole

The UK now spends more on debt interest than it does on schools, policing, or transport and working-age taxpayers foot the bill.

The debt interest payments in the UK for the fiscal year 2023–24 are projected to reach £78 billion. In the previous year, 2022–23, these payments soared to an unprecedented £108 billion, marking the highest level in the nation's history. It is important to note that these figures do not represent capital investments; instead, they constitute interest payments on past deficits.

A substantial portion of these payments is directed towards retirees, asset holders, and pension funds that hold inflation-linked government bonds, known as gilts. The cost of servicing debt interest now accounts for approximately 3% of the UK's GDP, which is higher than the nation's total education budget.

The impact of rising interest rates on debt costs is particularly alarming. According to projections made by the Office for Budget Responsibility (OBR), for every 1% increase in interest rates, the UK could see an additional £20 billion added to its debt costs by the year 2030. This escalating burden highlights the growing financial strain placed on working-age taxpayers and the urgent need to address this issue.

We’re being taxed to fund a system that pays debt interest to the people who least need it, and most benefit from inflation.

The Intergenerational Ledger

If this were a business, your generation would be subsidising everyone else’s dividends.

The young and working-age cohorts, defined as those aged 25 to 64, are significant net contributors to the fiscal system. Their economic activities and tax contributions provide the financial backbone that supports various societal expenditures. On the other hand, the retired cohorts, including individuals aged 65 to 74 and those over 75, are the primary beneficiaries of this system. Collectively, these retired groups receive over £200 billion in net transfers annually, highlighting the significant fiscal support directed toward them.

The Intergenerational Ledger: Net Fiscal Transfer by Age Group (2024 est.)

This Is Not Sustainable

The UK is headed for a fiscal cliff where rising debt, ageing costs, and tax exhaustion collide. And it’s our generation that will absorb the shock.

Key Pressure Points (OBR & Treasury forecasts, 2025–2030):

Tax burden to hit 38% of GDP by 2028, the highest since WWII

Working-age population shrinking, dependency ratio rising

State pension to exceed 6% of GDP by 2030, protected by triple lock

NHS demand rising faster than GDP, driven by chronic disease & ageing

Debt interest stays high (~£80bn/year), crowding out investment

Productivity flatlining and no growth engine to fund promises

2030 Scenarios:

Business-as-usual looks deceptively stable on paper: a tax-to-GDP ratio creeping past 40%, record receipts flowing into a system that delivers less each year, and a political class completely oblivious unless it impacts London.

Delayed reform is the same future, only faster. When markets blink, gilt yields spike, and when the cost of borrowing rises beyond what any spreadsheet had planned for, we will find ourselves cornered not by crisis, but by decades of avoidance. At that point, decisions will no longer feel like choices - they will arrive as inevitabilities: emergency cuts dressed up as discipline, pension reforms rushed through late-night votes, and another round of austerity, this time with even less credibility.

A productivity boom remains the only scenario in which we grow our way out of this morass, but despite all the rhetoric, we remain institutionally incapable of delivering it. The opportunities are real - AI, renewable energy, new forms of work and value etc. but the frameworks required to unlock them (education reform, housing availability, targeted investment, political vision) are either missing or actively obstructed.

And then there is rupture. The moment where managed decline gives way to unmanaged dissent. Intergenerational tension hardens into disengagement, disobedience, or something sharper. Young people stop turning up to vote, to participate, to believe. Others turn up differentlym angrier, more extreme, less willing to play by the rules of a game they never had a chance of winning. Trust decays, then collapses. And in its place: instability, flight, and the slow realisation that social contracts, once broken, do not mend on their own.

The truth is that no party has articulated a serious plan to drive long-term productivity, because doing so would require challenging the very constituencies they rely on to win power, and until that changes, the path to growth will remain technically possible, but politically blocked.

Now What?

The numbers don’t lie and now, neither can we. If we want a future that works, we need to demand one. Loudly and publicly.

We are living inside a system that was designed for a past that no longer exists.

And unless we challenge it, structurally, vocally, and soon, it will define the future we leave behind.

So what do we do?

Share this post - with your friends, your family, your colleagues, your MP.

Follow the campaign - Clarity in Chaos publishes new essays, data drops, tools, and strategic proposals every week.

Ask your MP a simple question: What are you doing to fix the intergenerational contract?

Something needs to change, clearly. Be apart of that change.

- AK x